Best 529 Plans for K-12 Private School Tuition: 2026 Rules After the $20K Bump

Paying private-school bills just got easier.

A July 2025 law doubled the annual K-12 withdrawal cap to $20,000 per child and widened “qualified expenses” to include tutoring, books, and test fees.

That bigger window turns the 529 from a college-only account into a flexible, tax-free wallet for kindergarten through high school.

Yet 529 plans aren’t created equal. Some states still tax K-12 withdrawals, while others couple low fees with quick, click-to-pay tools.

In this guide we rank the seven plans that maximize tax breaks, minimize costs, and speed tuition payments under the 2026 rules—so every dollar works harder for your family.

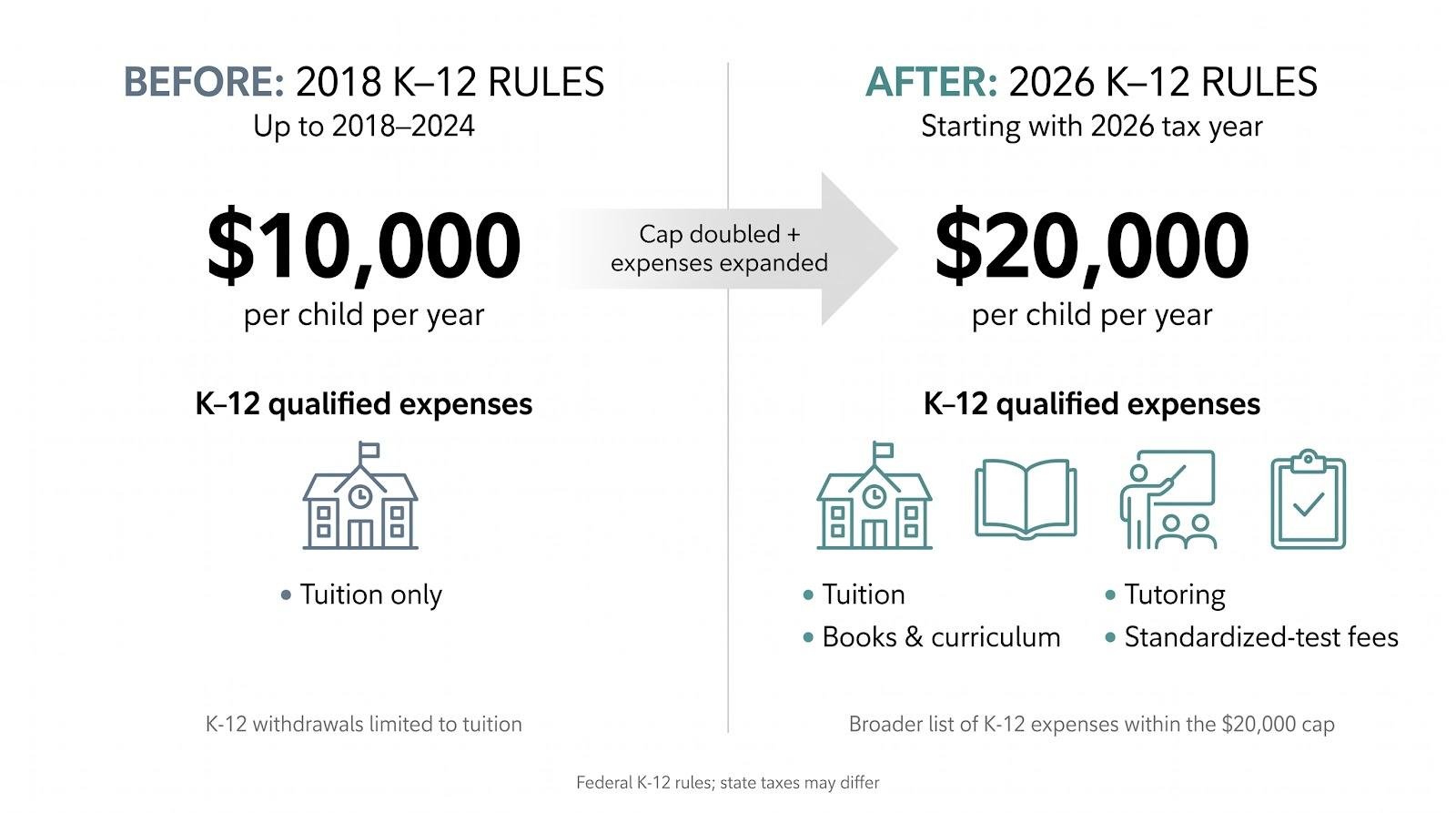

Why the new $20 000 limit matters

In 2018, 529 plans capped K-12 withdrawals at $10 000 and restricted them to tuition, leaving parents to pay for notebooks, test prep, and tutoring with after-tax cash.

A July 2025 law doubled that ceiling to $20 000 per child each year and broadened “qualified expenses” to include books, curriculum materials, tutoring, and standardized-test fees. The change applies starting with the 2026 tax year, giving families a larger, more flexible bucket.

That extra headroom matters. A higher allowance lets you pre-pay more of next year’s bill, so a larger balance compounds for several additional months. Over kindergarten through 12th grade, the growth can trim thousands from out-of-pocket costs.

The wider expense list solves another pain point: incidental costs that pop up each semester. The same tax-free dollars that handle tuition can now cover an AP exam or a weekly math tutor without triggering taxes or penalties.

Put simply, the new rule transforms a college-only account into a full-service education wallet. The rest of this guide shows which 529 plans protect those tax benefits while steering clear of state-level pitfalls.

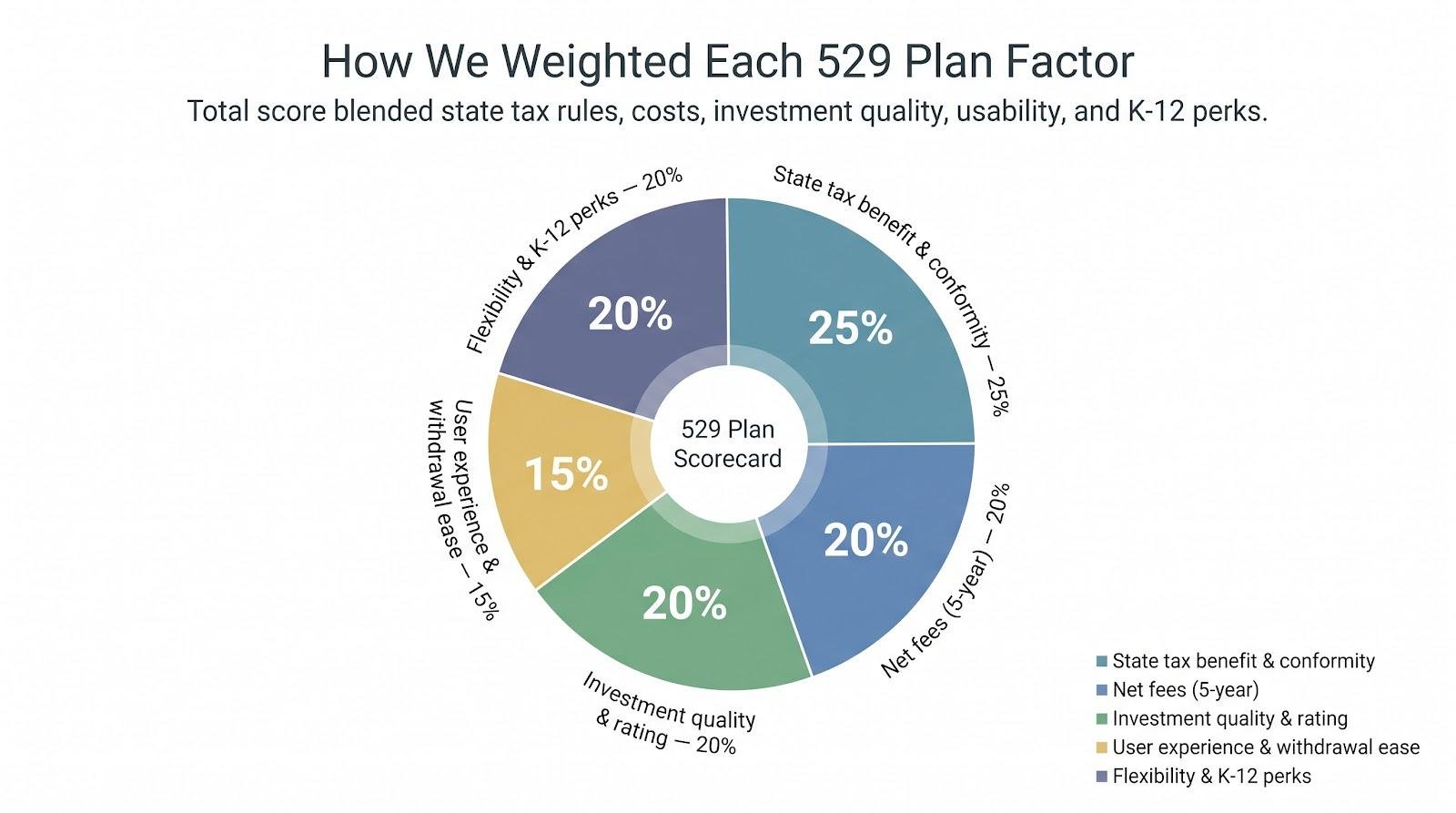

How we ranked the contenders

Choosing a 529 plan for private-school cash flow is part tax strategy, part investment decision, and part convenience. We weighed those factors, then ran every direct-sold plan through the same filter.

First, a plan had to come from a state that treats K-12 withdrawals as qualified or, at minimum, levies no income tax. Thirteen states, including California, Illinois, and New York, still ignore the federal rules by taxing earnings or recapturing deductions on K-12 distributions. Plans based in those states were penalized unless their other strengths offset the local hit for non-residents.

Next, we compared all-in costs. Low fees matter even more when your dollars may stay invested for only three to six years before middle-school bills arrive. We required at least one age-based or static index option priced at 0.40 percent or below.

Bright Start 529’s fee table lists a 0.10 percent total annual asset-based fee on its 2026 Enrollment portfolio, just one-quarter of our cu

On a $15 000 balance, that difference keeps about $45 a year working for your child instead of covering plan costs. Numbers like that helped lift Bright Start near the top of our scorecard.

Investment quality came third. Morningstar’s 2025 medal ratings and recent performance in moderate age-based tracks helped us separate thoughtful portfolio design from simple index tracking.

Finally, we scored everyday usability: online tools, withdrawal speed, and the ability to split money into short- and long-term sub-accounts. A plan that lets you schedule payments directly to the school always beat one that sends a paper check.

Weighting in practice looked like this:

State tax benefit and conformity – 25 percent

Net fees over a five-year horizon – 20 percent

Investment quality and rating – 20 percent

User experience and withdrawal ease – 15 percent

Flexibility plus K-12-specific perks – 20 percent

With the scorecard locked, only seven plans met the bar. The next section explains why the first plan leads the pack.

1. Bright Start (Illinois): lean fees, heavyweight results

If your goal is to keep more growth and pay fewer expenses, Bright Start sets the pace. Its index portfolios cost about 0.10 percent a year, almost negligible compared with the half-point drag many older plans still carry.

Independent analysts agree. Morningstar’s 2025 review placed Bright Start in its top tier, awarding the plan a Gold rating for “exceptional stewardship and investor-friendly pricing.”

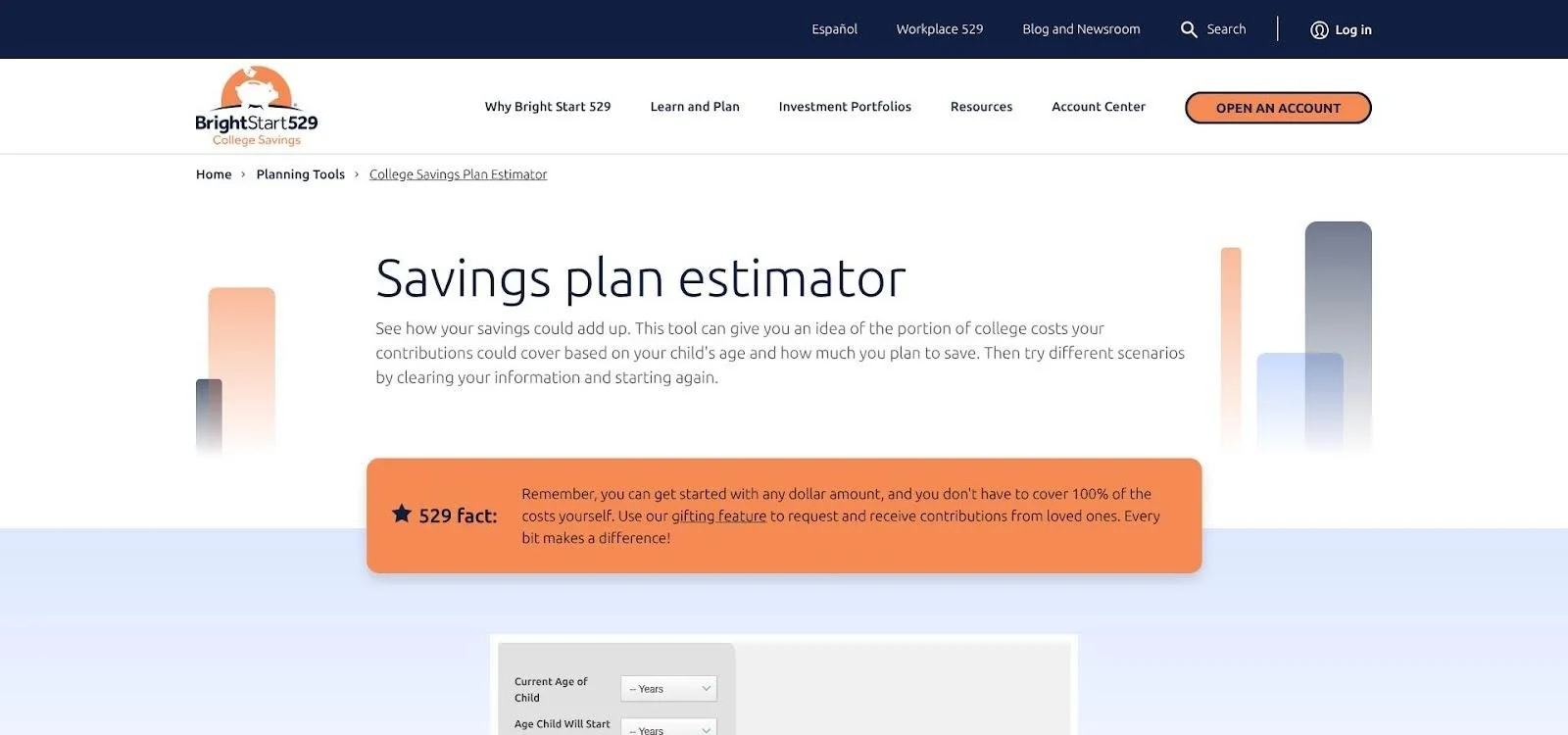

Navigation feels equally smooth. Illinois lets you rebalance or shift contributions online in minutes, and you can direct-pay many schools so money never detours through your checking account. The built-in College savings plan estimator doubles as a K-12 cash-flow tool; plug in your child’s grade to see whether you are on track for both eighth-grade tuition and freshman-year costs. Using the tool’s default assumptions of a 6 percent annual investment return and 5 percent yearly tuition growth, you can also test how far your current monthly contribution might stretch once college bills arrive.

Bright Start 529 college savings plan estimator tool screenshot

There is one pothole: Illinois is among the 13 states that still treat K-12 529 withdrawals as non-qualified for state tax purposes. If you live in-state and use Bright Start for private-school bills, Illinois will tax the earnings and claw back any prior state deduction. Out-of-state families avoid that hit, making Bright Start a smart pick for anyone seeking low costs without local penalties.

Choose Bright Start when you want market-matching growth at bargain pricing and you either live outside Illinois or are comfortable trading a small state tax bite for notable fee savings.

2. my529 (Utah): custom-built for short and long timelines

Utah’s direct-sold plan is a quiet standout that covers both elementary tuition and future college costs in one account.

Fees sit near the floor at about 0.12 percent on its most popular index tracks. The key feature is control. my529 lets you build a custom mix from Vanguard and DFA funds, then adjust that recipe twice a year. You can park next year’s tuition in a conservative sleeve while the rest of the balance stays growth-oriented for freshman-year expenses.

my529 Utah 529 plan homepage screenshot

Utah follows federal rules for K-12 withdrawals, and the state has no income tax on earnings, so every dollar you take for private school remains tax-free with no clawbacks or extra forms.

Daily use is straightforward. The dashboard shows separate goal buckets, letting you label one “Middle school” and another “College” and track each side by side. Need to pay this semester’s bill? A few clicks move the money to your checking account within three business days.

Pick my529 when you want Vanguard-level costs, spreadsheet-like flexibility, and zero state-tax friction in one plan.

3. Massachusetts U.Fund: Fidelity platform, index-level pricing

The Bay State’s U.Fund feels like placing your education savings inside a familiar Fidelity account. You log in with the same credentials you use for a 401(k) or brokerage account and move money around with simple drag-and-drop tools.

Costs stay friendly. Choose the Fidelity Index age-based track and you pay about 0.10 percent a year, matching the cheapest plans on our list. Prefer some active management? It is available, though the fee rises to roughly 0.80 percent.

Massachusetts fully follows the new K-12 rules, so any withdrawal up to the federal $20 000 cap is tax-free at the state level. Residents can also claim a modest deduction of up to $2 000 per couple each year and keep it when funds go to a private-school bursar.

Combine low index pricing with Fidelity’s polished mobile app and responsive customer support, and U.Fund becomes a solid choice for families seeking brand familiarity without high fees.

4. Pennsylvania 529 Investment Plan: tax-parity advantage

Pennsylvania gives residents a rare perk: a deduction for contributions to any 529 plan, not just the home option. That freedom already makes the PA 529 Investment Plan attractive, but the in-state offering is strong enough to keep your dollars parked right where you earn the deduction.

Vanguard manages the index lineup, so you get broad market exposure at roughly 0.25 percent in all-in costs. While not the cheapest on our list, the fee is reasonable once you factor in Pennsylvania’s generous deduction—up to $19 000 per child for single filers or $38 000 for couples each year.

The state adopted the full $20 000 K-12 rule with no clawbacks, so every withdrawal for private-school tuition stays tax-free locally. Stack that with the up-front deduction and you have a two-way win: save on taxes when you contribute and avoid taxes again when you pay the school.

Online, the interface is plain but effective. You can schedule one-time or recurring contributions, label multiple sub-accounts, and push payments out in less than a week. Customer service routes through the state treasury, and hold times are short.

Bottom line: If you live in Pennsylvania—or any tax-parity state—this plan deserves a close look. The combination of Vanguard stewardship, sizable deductions, and K-12 compliance can return real cash to your pocket.

5. Alaska 529: active management at a fair premium

Alaska has no state income tax, so the plan never questions how or when you spend 529 dollars. That blank slate lets it focus on one goal: seeking added returns through T. Rowe Price’s experienced managers.

Most age-based portfolios rely on active stock pickers who have topped their benchmarks more often than not. Fees sit above the index-only group at roughly 0.50 to 0.80 percent, but families with a five- to ten-year horizon may decide the potential extra gain offsets the cost. Even a one-percentage-point edge per year can outweigh the additional fee over eight semesters of tuition.

Getting started is simple. Open an account with 25 dollars, choose a glide path that matches your child’s graduation year, and set automatic contributions from a checking account or payroll. Need cash? Alaska usually processes electronic withdrawals within two business days. Because the state follows federal rules, every withdrawal up to the 20 000-dollar K-12 cap remains tax-free.

Pick Alaska 529 if you want professional stock selection and live in a state without strong home-state perks. The higher fee supports an investment team aiming to add value while you handle school runs and parent-teacher conferences.

6. New York 529 Direct: index purist’s pick with a local caveat

If your strategy is to own the whole market at the lowest cost, New York’s Direct Plan is hard to beat. Every portfolio, whether 100 percent stock or ultra-conservative bond, carries the same low expense of about 0.12 percent. No gimmicks, no tiered pricing—just plain Vanguard funds that hug their indexes closely. Morningstar’s 2025 report awarded the plan a Silver rating for solid stewardship.

The interface mirrors the simple lineup. Choose an age-based track or a static mix, set contributions, and you are done. The plan auto-rebalances and reduces risk as your child ages. Many parents treat it as a “set it and forget it” 529, a style that fits a busy school calendar.

Here is the catch: New York still taxes K-12 withdrawals. If you live in-state, earnings used for private-school tuition appear on your state return, and the deduction of up to 10 000 dollars for married couples is recaptured. Out-of-state investors avoid that penalty, enjoying low fees without New York taxes.

Use this plan if you live outside New York and want minimum costs, or if you are a New Yorker keeping 529 money reserved strictly for college. In both cases, the all-index approach lets more of your dollars keep compounding while you focus on homework instead of fund lineups.

7. Ohio CollegeAdvantage: deduction today, carry-forward tomorrow

Ohio’s direct-sold plan offers a strong mix many competitors miss: Vanguard and DFA funds, a 0.20–0.45 percent fee range, and a state tax break built for dedicated savers.

Key feature: residents may deduct up to $4 000 per child each year, and any contribution above that limit carries forward until fully used. Add $20 000 to the plan now and you lock in five years of state deductions—helpful when private-school tuition strains cash flow later.

Ohio fully conforms to the new $20 000 K-12 rule, so qualified withdrawals avoid state tax even if you invest in another state’s 529. That parity lets families claim the deduction while still comparison-shopping, though many stay because CollegeAdvantage’s age-based tracks have delivered solid long-term results.

Daily management is simple. Label sub-accounts by goal, automate transfers, and send payments to schools or your bank with a few clicks. Customer service answers quickly, a perk when a tuition bill is due Friday.

Choose Ohio CollegeAdvantage if you want mid-range fees, rollover-friendly tax savings, and the flexibility to front-load contributions without giving up future deductions.

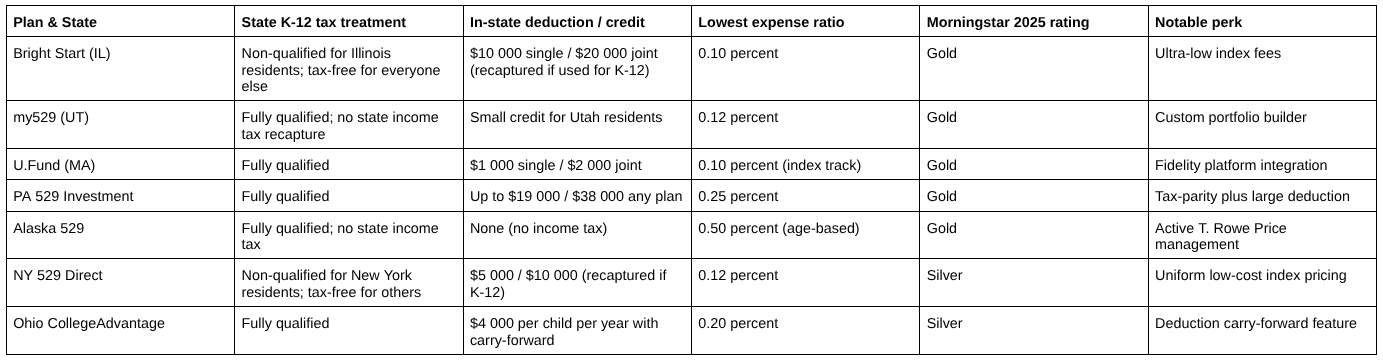

Compare the seven plans at a glance

All seven options meet our quality bar, but the differences become clear when you place them side by side. Scan the grid below, then focus on the column that matters most to you: state tax rules, fees, or investment strength.

Keep two questions front and center as you read the grid.

Will my state tax K-12 withdrawals?If so, consider an out-of-state plan that still meets your fee and service goals.

Which lever matters more right now: lower fees or a larger tax break?Fees erode growth quietly every year, while tax deductions put cash back in your pocket when you file. Balance both to match your timeline and comfort with risk.

With the comparison complete, the next section offers a quick decision guide to help you choose a plan in about a minute.

One-minute decision guide

I live in a conforming state and want the lowest fee. Choose New York Direct or Bright Start and keep withdrawals under the $20 000 cap.

My state taxes K-12 withdrawals. Open my529 or Alaska 529; both plans avoid state tax on earnings.

I need a large deduction right now. Pennsylvania residents can look to PA 529. Ohio residents can use CollegeAdvantage and front-load contributions to bank future carry-forwards.

I prefer familiar tools and live support.U.Fund pairs Fidelity’s interface with responsive customer service at a low cost.

Frequently asked questions

Can I really spend 529 money on tutoring now?

Yes. Federal law added tutoring, curriculum materials, and standardized-test fees to the qualified K-12 list in 2025. As long as your total K-12 withdrawals stay within the $20 000 annual cap per child, the earnings remain tax-free.

What if my state still taxes K-12 withdrawals?

You still enjoy federal tax-free status, but your home state may tax the earnings or recapture earlier deductions. If that applies to you, consider using a plan based in a conforming or no-tax state for private-school bills and keep a separate account for college, or pay tuition from cash flow or a Coverdell ESA.

Should I open two separate 529s—one for K-12 and one for college?

It is not required, but it can simplify bookkeeping. Keeping short-term tuition money in a conservative, separate account means you avoid selling growth assets during a market slump to cover next semester’s invoice.

What happens if I overfund the account?

Unused dollars can roll forward for college, graduate school, or even a sibling. Recent legislation also lets you move up to $35 000 into the beneficiary’s Roth IRA after fifteen years without a penalty.

Does the $20 000 limit adjust for inflation?

Not yet. Congress set a fixed cap, so everyone works with the same ceiling until lawmakers revisit the figure. That makes picking a low-fee, tax-efficient plan even more important because you want maximum growth on the dollars you can withdraw each year.

Conclusion

Pick the row that matches your priority, open the account today, and schedule your first automatic contribution before tomorrow’s school run. Your future self and your child’s teacher will appreciate the head start.

Related: