Can a Foreign Spouse Claim US Social Security?

Cross-border families face a retirement question that catches many of them off guard. American workers who have built up Social Security credits often assume their non-US spouse can automatically claim spousal or survivor benefits. The reality is more nuanced. Eligibility depends on the foreign spouse's country of residence, the relevant totalization or social-security agreement, and the specific benefit type being claimed.

Specialist firms provide the structured guidance these situations require. The Can a Foreign Spouse Claim U.S. Social Security? ebook from Cardinal Point Wealth Management walks through the eligibility framework. The right specialist reads the household's specific situation including citizenship, residency timeline, and country-of-residence rules.

Three structural realities make the foreign-spouse situation more complex than a typical Social Security claim. The first is the country-of-residence rule. The Social Security Administration restricts payment of benefits to non-US citizens in some countries.

The second is the totalization-agreement reality. The US has totalization agreements with about 30 countries that affect how foreign credits combine with US credits. The third is the survivor-benefit question. A foreign spouse claiming survivor benefits faces different eligibility rules than one claiming spousal benefits while the worker spouse is alive. The same long-horizon planning that informs how strong fathers invest in their relationships extends into the cross-border retirement conversation as the partnership reaches the planning years.

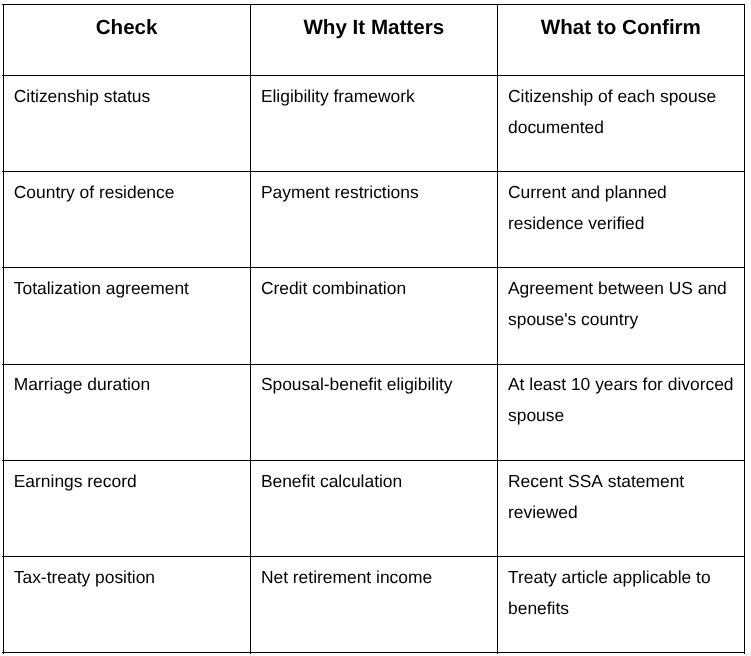

What Should Cross-Border Couples Verify Before Retirement?

Six checks belong on every cross-border couple's planning list. The table below summarises the priorities for households with mixed citizenship.

A planner who provides clear answers across these six points signals a specialist worth retaining. A planner who deflects on any of them often signals a generalist taking on cross-border work occasionally. The cost of asking these questions early is small relative to the cost of getting the retirement claim wrong.

Which Foreign-Spouse Scenarios Reward Specialist Counsel?

Three scenarios reward specialist depth more than the others. The first is the situation where the foreign spouse plans to remain in their home country while the US-citizen spouse retires. Country-of-residence rules determine whether benefits can be paid.

The second is the survivor-benefit scenario where the foreign spouse outlives the US-citizen spouse. The eligibility criteria differ from spousal benefits, and the residency requirements at the time of claim matter. The third is the divorced-foreign-spouse situation where a former spouse claims based on the US worker's record. The 10-year marriage-duration rule applies, but the foreign-spouse-specific rules layer on top.

The Social Security Administration's overview of payments to non-US citizens outlines the country-of-residence framework. The SSA's overview of totalization agreements covers the credit-combination rules. Specialist planning starts where these government guides end and applies the rules to the household's specific facts.

What Common Mistakes Surface in Cross-Border Retirement Planning?

Several patterns recur. The first is assuming spousal benefits are automatic. The application process requires documentation that takes time to assemble.

The second is overlooking the country-of-residence restriction. Some countries' residents face payment suspension after extended absence from the United States.

The third is treating divorced-spouse claims casually. The 10-year marriage rule has specific requirements that must be documented carefully. The fourth is forgetting the tax-treatment of US Social Security in the foreign country. Some treaties allocate taxation to the country of residence, others to the country of payment. The fifth is improvising the timing of the claim without coordinating with the worker spouse's own claim timing.

The sixth is treating retirement-side decisions in isolation from the day-to-day household balance the way work-life balance discussions for busy dads recommend. Cross-border couples who fold the retirement-planning conversation into the regular household-finance routine produce calmer outcomes than couples who batch it into a stressful pre-retirement scramble.

What Is the Bottom Line for Cross-Border Couples?

The foreign-spouse Social Security decision rewards couples who plan rather than improvise. The window for thoughtful preparation typically runs across the 10 to 15 years before retirement. The right specialist coordinates the citizenship situation, the residency planning, and the benefit-timing decisions rather than treating each as a separate question.

Whether the household plans US retirement, foreign retirement, or split-time retirement, the criteria translate cleanly. The first conversation should answer specific questions about eligibility, country-of-residence rules, and projected outcomes. Couples who run real planning early end up with cleaner retirement outcomes than those who default to the standard advice that does not fit their specific situation. The geography differs across households but the homework discipline does not.

Frequently Asked Questions

Can a Foreign Spouse Claim US Spousal Benefits Without Living in the US?

Sometimes. Country-of-residence rules apply. Some countries' residents face full or partial payment restrictions. The SSA's country-by-country rules determine whether benefits flow without restriction or with restriction. Verify the spouse's country of residence before any planning assumption.

What Is the Marriage-Duration Requirement for Spousal Benefits?

Currently married spouses qualify for spousal benefits at retirement age based on the worker spouse's record. Divorced spouses qualify based on at least 10 years of marriage to the worker, plus other criteria. Surviving spouses qualify based on at least 9 months of marriage in most cases. The exceptions cover situations where the worker died accidentally or in military service.

How Does the Totalization Agreement Affect Foreign Spouses?

The agreement primarily helps the spouse who has worked in both countries. For a spouse who never worked in the US, totalization rules do not directly apply. The spouse claims under standard spousal or survivor rules, with country-of-residence restrictions layered on top. Couples with mixed work histories should verify the agreement's specifics for their country pairing.

When Should I Engage a Cross-Border Specialist?

Engage a specialist 10 to 15 years before retirement, or as soon as the cross-border situation arises. Pre-retirement planning, the documentation work, and the strategic-claim-timing decisions all benefit from time. Last-minute consultations limit the planning options. The first conversation usually carries no fee or a modest engagement charge.